Are Better Days Ahead for C-store Real Estate?

In a previous column, I noted the 44-percent decline in convenience store real estate prices since the peak in 2006. During the same period, pretax profits have been on the increase. If industry pre-tax profits are rising, why did real estate prices decline?

In a previous column, I noted the 44-percent decline in convenience store real estate prices since the peak in 2006. During the same period, pretax profits have been on the increase. If industry pre-tax profits are rising, why did real estate prices decline?

Pretax profit is the economic motivation for buyers to enter the convenience industry. As more buyers enter because of higher pretax profits, demand for real estate grows. This increasing demand should cause prices to rise because supply is relatively fixed over the short-run. This is simple economics.

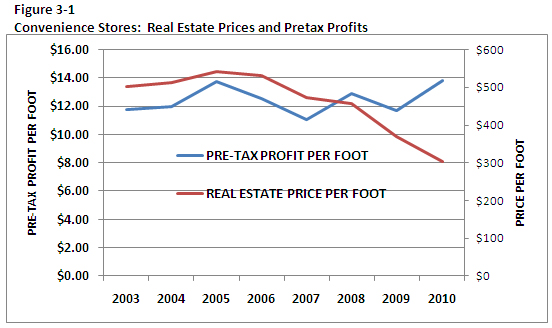

Perhaps we can learn more by looking at the long-term trends over the last decade. Figure 3-1 shows the relationship between real estate prices and pretax profits. Both are expressed on a per-square-foot basis. From 2003 to 2007 the relationship was very consistent. When pretax profits rose and fell, so did real estate prices. Over this period, the multiple of convenience store real estate prices to pretax profit was around 40. However, in 2008, this relationship changed. When the "Great Recession" began, real estate prices fell (red line), while pretax profits continued to rise (blue line).

As can be seen in Figure 3-2, the real estate price to pretax profit multiple declined from 43 in 2007 to 35 in 2008, 32 in 2009, and finally to 22 in 2010. Today's multiple has dropped 49 percent from the 2003-to-2007 period.

The increase in pretax profits was not caused by lower occupancy costs resulting from the decline in real estate prices, because the increase in pretax profits from 2003 to 2010 shows a consistent pattern of following the trend in gross margin. In other words, higher levels of gross margin led to these higher pretax profits.

These long-term relationships show us that the drop in convenience store real estate prices over the last decade appears to be a result of the overall decline in commercial real estate prices brought about by the Great Recession, not as a result of the economics of the convenience retail industry over this period.

So, when convenience store real estate prices correct, they should move upward. Based on the trend in pretax profit, convenience store real estate prices should rebound from the $302-per-square-foot level in 2010 to the $550-per-square-foot range. This would be an 82 percent increase from today's pricing points.

The next question is: when? I expect it will be sooner rather than later because real estate prices have already been in disequilibrium for two years. This is a pent-up pricing correction. As soon as the national economy begins to stabilize, this price correction will break out rapidly.

From what we know now, better days are ahead for convenience store real estate prices.

Robert E. Bainbridge is an author, instructor and expert witness in the appraisal and valuation of convenience stores and gas stations. He can be reached at [email protected] or (541) 823-0029. Find more valuation information at www.cstorevalue.com.

Editor's Note: The opinions expressed in this column are the author's, and do not necessarily reflect the views of Convenience Store News.